p-values#

Links: notebook, html, PDF, python, slides, GitHub

Compute p-values and heavy tails estimators.

from jyquickhelper import add_notebook_menu

add_notebook_menu()

%matplotlib inline

p-value table#

from scipy.stats import norm

import pandas

from pandas import DataFrame

import numpy

def pvalue(p, q, N):

theta = abs(p-q)

var = p*(1-p)

bn = (2*N)**0.5 * theta / var**0.5

ret = (1 - norm.cdf(bn))*2

return ret

def pvalue_N(p, q, alpha):

theta = abs(p-q)

var = p*(1-p)

rev = abs(norm.ppf (alpha/2))

N = 2 * (rev * var**0.5 / theta)** 2

return int(N+1)

def alphatable(ps, dps, alpha):

values = []

for p in ps :

row=[]

for dp in dps :

q = p+dp

r = pvalue_N(p,q,alpha) if 1 >= q >= 0 else numpy.nan

row.append (r)

values.append (row)

return values

def dataframe(ps,dps,table):

columns = dps

df = pandas.DataFrame(data=table, index=ps)

df.columns = dps

return df

print ("norm.ppf(0.025)",norm.ppf (0.025)) # -1.9599639845400545

ps = [0.001, 0.002] + [ 0.05*i for i in range (1,20) ]

dps = [ -0.2, -0.1, -0.02, -0.01, -0.002, -0.001,

0.2, 0.1, 0.02, 0.01, 0.002, 0.001, ]

dps.sort()

t = alphatable(ps, dps, 0.05)

dataframe (ps, dps, t)

norm.ppf(0.025) -1.9599639845400545

| -0.200 | -0.100 | -0.020 | -0.010 | -0.002 | -0.001 | 0.001 | 0.002 | 0.010 | 0.020 | 0.100 | 0.200 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.001 | NaN | NaN | NaN | NaN | NaN | 7676 | 7676 | 1919 | 77 | 20 | 1.0 | 1.0 |

| 0.002 | NaN | NaN | NaN | NaN | 3834.0 | 15336 | 15336 | 3834 | 154 | 39 | 2.0 | 1.0 |

| 0.050 | NaN | NaN | 913.0 | 3650.0 | 91235.0 | 364939 | 364939 | 91235 | 3650 | 913 | 37.0 | 10.0 |

| 0.100 | NaN | 70.0 | 1729.0 | 6915.0 | 172866.0 | 691463 | 691463 | 172866 | 6915 | 1729 | 70.0 | 18.0 |

| 0.150 | NaN | 98.0 | 2449.0 | 9796.0 | 244893.0 | 979572 | 979572 | 244893 | 9796 | 2449 | 98.0 | 25.0 |

| 0.200 | 31.0 | 123.0 | 3074.0 | 12293.0 | 307317.0 | 1229267 | 1229267 | 307317 | 12293 | 3074 | 123.0 | 31.0 |

| 0.250 | 37.0 | 145.0 | 3602.0 | 14406.0 | 360137.0 | 1440548 | 1440548 | 360137 | 14406 | 3602 | 145.0 | 37.0 |

| 0.300 | 41.0 | 162.0 | 4034.0 | 16135.0 | 403354.0 | 1613413 | 1613413 | 403354 | 16135 | 4034 | 162.0 | 41.0 |

| 0.350 | 44.0 | 175.0 | 4370.0 | 17479.0 | 436966.0 | 1747864 | 1747864 | 436966 | 17479 | 4370 | 175.0 | 44.0 |

| 0.400 | 47.0 | 185.0 | 4610.0 | 18440.0 | 460976.0 | 1843901 | 1843901 | 460976 | 18440 | 4610 | 185.0 | 47.0 |

| 0.450 | 48.0 | 191.0 | 4754.0 | 19016.0 | 475381.0 | 1901523 | 1901523 | 475381 | 19016 | 4754 | 191.0 | 48.0 |

| 0.500 | 49.0 | 193.0 | 4802.0 | 19208.0 | 480183.0 | 1920730 | 1920730 | 480183 | 19208 | 4802 | 193.0 | 49.0 |

| 0.550 | 48.0 | 191.0 | 4754.0 | 19016.0 | 475381.0 | 1901523 | 1901523 | 475381 | 19016 | 4754 | 191.0 | 48.0 |

| 0.600 | 47.0 | 185.0 | 4610.0 | 18440.0 | 460976.0 | 1843901 | 1843901 | 460976 | 18440 | 4610 | 185.0 | 47.0 |

| 0.650 | 44.0 | 175.0 | 4370.0 | 17479.0 | 436966.0 | 1747864 | 1747864 | 436966 | 17479 | 4370 | 175.0 | 44.0 |

| 0.700 | 41.0 | 162.0 | 4034.0 | 16135.0 | 403354.0 | 1613413 | 1613413 | 403354 | 16135 | 4034 | 162.0 | 41.0 |

| 0.750 | 37.0 | 145.0 | 3602.0 | 14406.0 | 360137.0 | 1440548 | 1440548 | 360137 | 14406 | 3602 | 145.0 | 37.0 |

| 0.800 | 31.0 | 123.0 | 3074.0 | 12293.0 | 307317.0 | 1229267 | 1229267 | 307317 | 12293 | 3074 | 123.0 | 31.0 |

| 0.850 | 25.0 | 98.0 | 2449.0 | 9796.0 | 244893.0 | 979572 | 979572 | 244893 | 9796 | 2449 | 98.0 | NaN |

| 0.900 | 18.0 | 70.0 | 1729.0 | 6915.0 | 172866.0 | 691463 | 691463 | 172866 | 6915 | 1729 | 70.0 | NaN |

| 0.950 | 10.0 | 37.0 | 913.0 | 3650.0 | 91235.0 | 364939 | 364939 | 91235 | 3650 | 913 | NaN | NaN |

p-values in 2D#

import numpy, matplotlib, random, math

import matplotlib.pyplot as pylab

def matrix_square_root(sigma) :

eigen, vect = numpy.linalg.eig(sigma)

dim = len(sigma)

res = numpy.identity(dim)

for i in range(0,dim) :

res[i,i] = eigen[i]**0.5

return vect * res * vect.transpose()

def chi2_level (alpha = 0.95) :

N = 1000

x = [ random.gauss(0,1) for _ in range(0,N) ]

y = [ random.gauss(0,1) for _ in range(0,N) ]

r = map ( lambda c : (c[0]**2+c[1]**2)**0.5, zip(x,y))

r = list(r)

r.sort()

res = r [ int (alpha * N) ]

return res

def square_figure(mat, a) :

x = [ ]

y = [ ]

for i in range (0,100) :

x.append( a * mat[0][0]**0.5 )

y.append( (random.random ()-0.5) * a * mat[1][1]**0.5*2 )

x.append( -a * mat[0][0]**0.5 )

y.append( (random.random ()-0.5) * a * mat[1][1]**0.5*2 )

y.append( a * mat[1][1]**0.5 )

x.append( (random.random ()-0.5) * a * mat[0][0]**0.5*2 )

y.append( -a * mat[1][1]**0.5 )

x.append( (random.random ()-0.5) * a * mat[0][0]**0.5*2 )

pylab.plot(x,y, 'ro')

x = [ ]

y = [ ]

for i in range (0,100) :

x.append( a )

y.append( (random.random ()-0.5) * a*2 )

x.append( -a )

y.append( (random.random ()-0.5) * a*2 )

y.append( a )

x.append( (random.random ()-0.5) * a*2 )

y.append( -a )

x.append( (random.random ()-0.5) * a*2 )

xs,ys = [],[]

for a,b in zip (x,y) :

ar = numpy.matrix( [ [a], [b] ] ).transpose()

we = ar * root

xs.append( we [0,0] )

ys.append( we [0,1] )

pylab.plot(xs,ys, 'bo')

pylab.show()

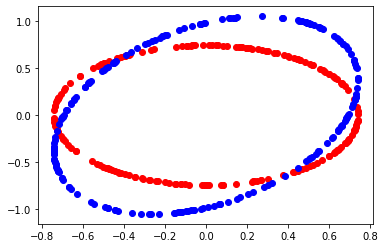

def circle_figure (mat, a) :

x = [ ]

y = [ ]

for i in range (0,200) :

z = random.random() * math.pi * 2

i = a * mat[0][0]**0.5 * math.cos(z)

j = a * mat[0][0]**0.5 * math.sin(z)

x.append ( i )

y.append ( j )

pylab.plot(x,y, 'ro')

x = [ ]

y = [ ]

for i in range (0,200) :

z = random.random() * math.pi * 2

i = a * math.cos(z)

j = a * math.sin(z)

x.append ( i )

y.append ( j )

xs,ys = [],[]

for a,b in zip (x,y) :

ar = numpy.matrix( [ [a], [b] ] ).transpose()

we = ar * root

xs.append( we [0,0] )

ys.append( we [0,1] )

pylab.plot(xs,ys, 'bo')

pylab.show()

level = chi2_level ()

mat = [ [0.1, 0.05], [0.05, 0.2] ]

npmat = numpy.matrix(mat)

root = matrix_square_root (npmat)

square_figure (mat, 1.96)

circle_figure (mat, level)

p-value ratio#

import random, math

def densite_gauss (mu, sigma, x) :

e = -(x - mu)**2 / (sigma**2 * 2)

d = 1. / ((2*math.pi)**0.5 * sigma)

return d * math.exp (e)

def simulation_vector (N, mu, sigma) :

return [ random.gauss(mu,sigma) for n in range(N) ]

def ratio (vector, x, fdensite) :

under = 0

above = 0

fx = fdensite(x)

for u in vector:

f = fdensite (u)

if f >= fx:

above += 1

else:

under += 1

return float(above) / float (above + under)

x = 1.96

N = 10000

mu = 0

sigma = 1

v = simulation_vector(N, mu, sigma)

g = ratio(v, x, lambda y: densite_gauss (mu, sigma, y) )

print (g)

0.9487

p-values and EM#

See Applying the EM Algorithm: Binomial Mixtures.

from scipy.stats import norm

import random, math

def average_std_deviation(sample):

mean = 0.

var = 0.

for x in sample:

mean += x

var += x*x

mean /= len(sample)

var /= len(sample)

var -= mean*mean

return mean,var ** 0.5

def bootsample(sample):

n = len(sample)-1

return [ sample[ random.randint(0,n) ] for _ in sample ]

def bootstrap_difference(sampleX, sampleY, draws=2000, confidence=0.05):

diff = [ ]

for n in range (0,draws) :

if n % 1000 == 0:

print(n)

sx = bootsample(sampleX)

sy = bootsample(sampleY)

px = sum(sx) * 1.0/ len(sx)

py = sum(sy) * 1.0/ len(sy)

diff.append (px-py)

diff.sort()

n = int(len(diff) * confidence / 2)

av = sum(diff) / len(diff)

return av, diff [n], diff [len(diff)-n]

# generation of a sample

def generate_obs(p):

x = random.random()

if x <= p : return 1

else : return 0

def generate_n_obs(p, n):

return [ generate_obs(p) for i in range (0,n) ]

# std deviation

def diff_std_deviation(px, py):

s = px*(1-px) + py*(1-py)

return px, py, s**0.5

def pvalue(diff, std, N):

theta = abs(diff)

bn = (2*N)**0.5 * theta / std

pv = (1 - norm.cdf(bn))*2

return pv

def omega_i (X, pi, p, q) :

np = p * pi if X == 1 else (1-p)*pi

nq = q * (1-pi) if X == 1 else (1-q)*(1-pi)

return np / (np + nq)

def likelihood (X, pi, p, q) :

np = p * pi if X == 1 else (1-p)*pi

nq = q * (1-pi) if X == 1 else (1-q)*(1-pi)

return math.log(np) + math.log(nq)

def algoEM (sample):

p = random.random()

q = random.random()

pi = random.random()

iter = 0

while iter < 10 :

lk = sum ( [ likelihood (x, pi, p, q) for x in sample ] )

wi = [ omega_i (x, pi, p, q) for x in sample ]

sw = sum(wi)

pin = sum(wi) / len(wi)

pn = sum([ x * w for x,w in zip (sample,wi) ]) / sw

qn = sum([ x * (1-w) for x,w in zip (sample,wi) ]) / (len(wi) - sw)

pi,p,q = pin,pn,qn

iter += 1

lk = sum ( [ likelihood (x, pi, p, q) for x in sample ] )

return pi,p,q, lk

# mix

p,q = 0.20, 0.80

pi = 0.7

N = 1000

na = int(N * pi)

nb = N - na

print("------- sample")

sampleX = generate_n_obs(p, na) + generate_n_obs (q, nb)

random.shuffle(sampleX)

print("ave", p * pi + q*(1-pi))

print("mea", sum(sampleX)*1./len(sampleX))

lk = sum ( [ likelihood (x, pi, p, q) for x in sampleX ] )

print ("min lk", lk, sum (sampleX)*1. / len(sampleX))

res = []

for k in range (0, 10) :

r = algoEM (sampleX)

res.append ( (r[-1], r) )

res.sort ()

rows = []

for r in res:

pi,p,q,lk = r[1]

rows.append( [p * pi + q*(1-pi)] + list(r[1]))

df = pandas.DataFrame(data=rows)

df.columns = ["average", "pi", "p", "q", "likelihood"]

df

------- sample

ave 0.38

mea 0.373

min lk -3393.2292120130046 0.373

| average | pi | p | q | likelihood | |

|---|---|---|---|---|---|

| 0 | 0.373 | 0.000324 | 0.341877 | 0.373010 | -9358.705695 |

| 1 | 0.373 | 0.863747 | 0.284788 | 0.932204 | -4531.967709 |

| 2 | 0.373 | 0.936083 | 0.346101 | 0.766941 | -4490.512057 |

| 3 | 0.373 | 0.123023 | 0.290964 | 0.384508 | -3563.557269 |

| 4 | 0.373 | 0.538835 | 0.053584 | 0.746213 | -3487.438442 |

| 5 | 0.373 | 0.346351 | 0.057880 | 0.539974 | -3302.391944 |

| 6 | 0.373 | 0.797540 | 0.376491 | 0.359248 | -3144.938682 |

| 7 | 0.373 | 0.392520 | 0.592563 | 0.231131 | -2902.915478 |

| 8 | 0.373 | 0.390241 | 0.459488 | 0.317648 | -2778.903072 |

| 9 | 0.373 | 0.609127 | 0.338062 | 0.427447 | -2764.987703 |

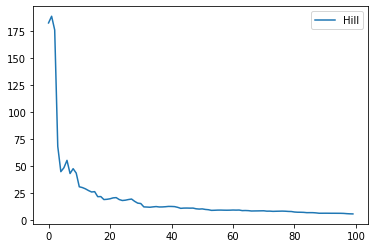

p-value and heavy tail#

from scipy.stats import norm, zipf

import sys

def generate_n_obs_zipf (tail_index, n) :

return list(zipf.rvs(tail_index, size=n))

def hill_estimator (sample) :

sample = list(sample)

sample.sort(reverse=True)

end = len(sample)/10

end = min(end,100)

s = 0.

res = []

for k in range (0,end) :

s += math.log(sample[k])

h = (s - (k+1)*math.log(sample[k+1]))/(k+1)

h = 1./h

res.append( [k, h] )

return res

# mix

tail_index = 1.05

N = 10000

sample = generate_n_obs_zipf(tail_index, N)

sample[:5]

[357621, 148, 18, 1812876449, 36150]

import pandas

def graph_XY(curves, xlabel=None, ylabel=None, marker=True,

link_point=False, title=None, format_date="%Y-%m-%d",

legend_loc=0, figsize=None, ax=None):

if ax is None:

import matplotlib.pyplot as plt # pylint: disable=C0415

fig, ax = plt.subplots(1, 1, figsize=figsize)

smarker = {(True, True): 'o-', (True, False): 'o', (False, True): '-',

# (False, False) :''

}[marker, link_point]

has_date = False

for xf, yf, label in curves:

ax.plot(xf, yf, smarker, label=label)

ax.legend(loc=legend_loc)

return ax

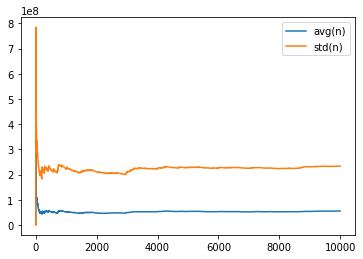

def draw_variance(sample) :

avg = 0.

std = 0.

n = 0.

w = 1.

add = []

for i,x in enumerate(sample) :

x = float (x)

avg += x * w

std += x*x * w

n += w

val = (std/n - (avg/n)**2)**0.5

add.append ( [ i, avg/n, val] )

print(add[-1])

table = pandas.DataFrame(add, columns=["index", "avg(n)", "std(n)"])

return graph_XY([

[table['index'], table["avg(n)"], "avg(n)"],

[table['index'], table["std(n)"], "std(n)"],

], marker=False, link_point=True)

draw_variance(sample);

[9999, 55186871.0339, 233342554.46156308]

def draw_hill_estimator (sample) :

res = hill_estimator(sample)

table = DataFrame(res, columns=["d", "hill"])

return graph_XY(

[[table['d'], table['hill'], "Hill"],],

marker=False, link_point=True)

draw_hill_estimator(sample);

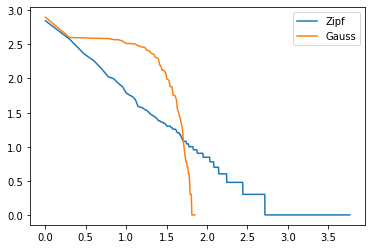

def draw_heavy_tail (sample) :

table = DataFrame([[_] for _ in sample ], columns=["obs"])

std = 1

normal = norm.rvs(size = len(sample))

normal = [ x*std for x in normal ]

nortbl = DataFrame([ [_] for _ in normal ], columns=["obs"])

nortbl["iobs"] = (nortbl['obs'] * 10).astype(numpy.int64)

histon = nortbl[["iobs", "obs"]].groupby('iobs', as_index=False).count()

histon.columns = ['iobs', 'nb']

histon = histon.sort_values("nb", ascending=False).reset_index(drop=True)

table["one"] = 1

histo = table.groupby('obs', as_index=False).count()

histo.columns = ['obs', 'nb']

histo = histo.sort_values('nb', ascending=False).reset_index(drop=True)

histo.reset_index(drop=True, inplace=True)

histo["index"] = histo.index + 1

vec = list(histon["nb"])

vec += [0,] * len(histo)

histo['nb_normal'] = vec[:len(histo)]

histo["log(index)"] = numpy.log(histo["index"]) / numpy.log(10)

histo["log(nb)"] = numpy.log(histo["nb"]) / numpy.log(10)

histo["log(nb_normal)"] = numpy.log(histo["nb_normal"]) / numpy.log(10)

return graph_XY ([

[histo["log(index)"], histo["log(nb)"], "Zipf"],

[histo["log(index)"], histo["log(nb_normal)"], "Gauss"], ],

marker=False, link_point=True)

draw_heavy_tail(sample);

c:python372_x64libsite-packagespandascoreseries.py:679: RuntimeWarning: divide by zero encountered in log result = getattr(ufunc, method)(*inputs, **kwargs)